[ad_1]

Fintech is booming in Australia! The sector is now price round $45billion AUS (over $30billion USD) – a 17900 per cent rise from 2015’s worth ($250billion AUS/$168million USD) in accordance with Fintech Australia. However what subsectors are main the best way and may the nation sustain its development?

First, let’s take a step again and have a look at the monetary panorama in Australia extra usually. Regardless of its market stalling in H1’24, Australia’s financial system nonetheless stays a serious participant globally with a gross home product (GDP) per capita of over $65,000 in accordance with the World Financial institution.

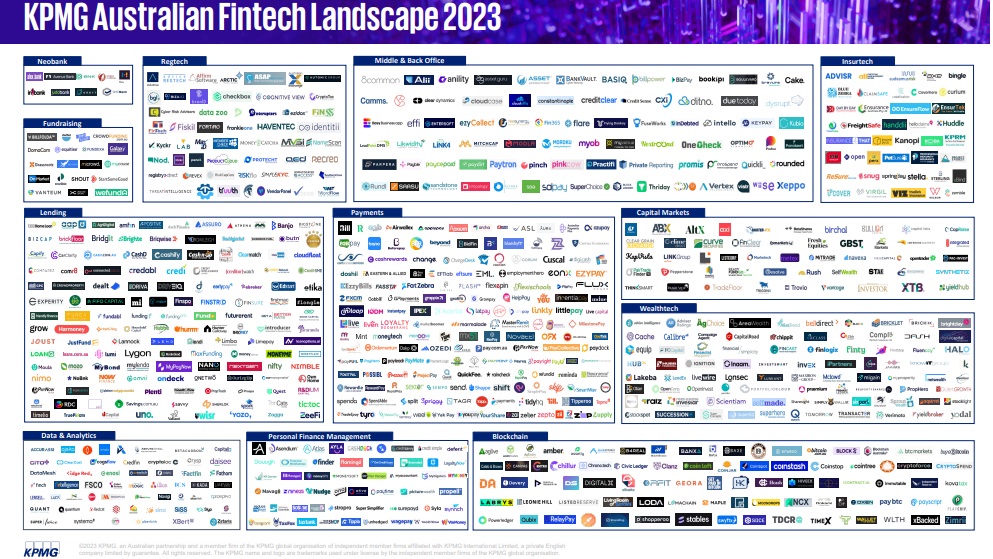

In response to the KPMG Fintech Panorama 2023, the ecosystem could be very various in Australia with over 830 unbiased fintechs headquartered within the area.

The fintech panorama

The Australian state of New South Wales, house to the nation’s capital, has the biggest proportion of fintech firms (60 per cent). That is adopted by Victoria (24 per cent) and Queensland (12 per cent).

The nation can be house to numerous unicorns. These embody cross-border funds Airwallex, purchase now pay later (BNPL) Afterpay and challenger financial institution Judo Capital.

The funds subsector is the biggest in Australia. It has a 20 per cent share of all fintechs within the nation with over 160 corporations. Lending and wealthtech take second and third place respectively. Lending represents 17 per cent of the market (140 fintechs), whereas wealthtech represents 10 per cent.

Open banking is one other notable subsector in Australia. Nearly all of the APAC area’s adoption of the expertise has been market-driven – nevertheless, in Australia, laws have pushed its improvement. This was evident in July 2019, when Australia launched its open banking regime, primarily based on shopper knowledge proper (CDR) laws. The regime’s purpose was to offer clients extra management over their knowledge and simpler entry to services and products they required.

There have been different milestones in 2019 too. For instance, main banks celebrated software programming interfaces (APIs) and eligible product knowledge, comparable to charges, charges, and phrases and circumstances. A 12 months later, particular person account holders and sole merchants might share knowledge regarding their retail banking merchandise.

In 2021, knowledge sharing was additional improved as clients might share info enterprise lending, belief accounts, overdrafts, asset finance, traces of credit score and international forex accounts. Moreover, main banks allowed for knowledge sharing for non-individuals, secondary customers and enterprise partnerships.

Latest information

Australia was not capable of escape the declines in fintech funding skilled internationally. When it comes to deal exercise, it noticed a 61.9 per cent decline from 42 offers in Q2’23 to 16 in QR’24. From a funding standpoint, there was additionally a drop because the nation raised $475million in Q2’24 which was 73.5 per cent decrease than Q2’23 ($1.8billion).

In response to Fintech Australia’s fourth version of its Australian Open Banking Ecosystem Map and Report, which was supported by Mastercard, and in partnership with FinTech NZ, Funds NZ and Open Finance ANZ, the nation noticed a 165 per cent improve in shopper knowledge proper (CDR) individuals. Different findings revealed that just about all shopper financial institution accounts (99.74 per cent) are actually related to the open banking ecosystem, positioning Australia for additional adoption of open banking applied sciences.

Final month, the Australian authorities proposed the introduction of a Scams Prevention Framework (SPF), implementing new obligatory rip-off obligations throughout all sectors. The Invoice, which might insert the SPF into the ‘Competitors and Shopper Act 2010,’ is predicted to be launched to the federal parliament subsequent month.

[ad_2]

Source link